This article focuses on Corporate Tax Administration in Indonesia and talks about various deadlines for companies, tax incentives, tax audits and penalties for non-compliance.

As per Indonesian tax law, if a company has a permanent establishment (PE) or domicile in Indonesia, it is considered a resident in Indonesia for tax purposes. A resident company is subject to tax obligations in Indonesia whereby it is required to make the tax payments to the State Treasury and then file the tax returns with the Directorate General of Tax (DGIT). Some taxes are paid and filed monthly while others are paid and filed annually the details of which are given below.

Companies can settle some of their tax obligations electronically through corporate bank accounts while other tax obligations are settled in the form of third-party withholdings. Monthly tax payments by companies are considered as the prepayment towards their current year total CIT liability and these monthly payments are based on the most recent CIT return. The tax withheld by third parties on certain income is also considered as the prepayment for the current year tax liability. If the total amount of tax directly paid or withheld by the third parties falls short of the total liability at the year-end, the company must settle the shortfall before filing the CIT return.

A summary of these tax obligations is as follows:

Monthly tax obligations

| Type of tax |

Tax payment deadline |

Tax return filing deadline |

| Article 21/26 (Payroll) WHT |

The 10th day of the following month |

20th day of the following month |

| Article 23/26 Income Tax |

The 10th day of the following month |

20th day of the following month |

| Article 25 Income Tax Instalment |

The 15th day of the following month |

20th day of the following month |

| Article 22 Income Tax on imports/payments to Tax Collectors |

The 10th day of the following month |

20th day of the following month |

| Article 4(2) Final Income Tax |

The 10th day of the following month |

20th day of the following month |

| VAT and LST |

Prior to the tax return filing deadline |

The end of the following month |

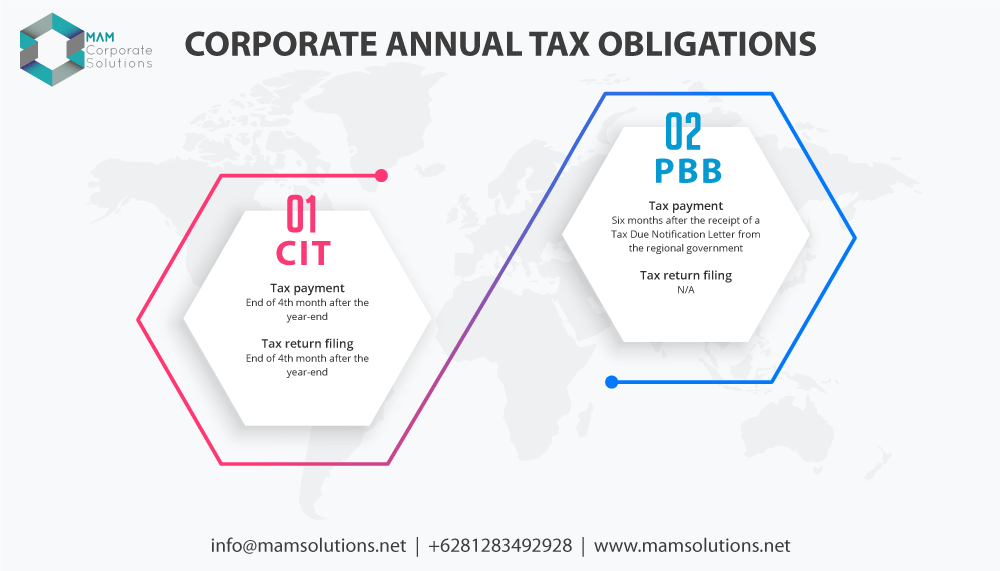

Annual tax obligations

| Type of tax |

Tax payment deadline |

Tax return filing deadline |

| CIT |

The end of the fourth month after the book year-end before filing the tax return |

The end of the fourth month after the book year-end |

| PBB |

Six months after the receipt of a Tax Due Notification Letter from the regional government |

N/A |

Penalties for the late payment

Proper corporate tax administration is important, and companies are subject to penalties for late or non-payment of taxes. It is important to note that the penalties are charged on monthly basis and even if a company has delayed tax payment by just one day, it will be considered as one full month.

The penalties for late filing of tax returns are given below:

| Type of tax return |

IDR |

| VAT return |

500,000 |

| Other monthly tax returns |

100,000 |

| CIT return |

1,000,000 |

Tax assessment

Indonesia follows the self-assessment tax system of corporate tax administration which places the responsibility of correctly calculating and payment of the tax liability on the taxpayer. However, DGT can anytime intervene and ask for an explanation if it finds out that the company is not fully paying its tax liabilities.

It is therefore very important to ensure that taxpayers correctly calculate and pay the tax liabilities. DGT may also ask for an explanation if the company has not maintained the books as per the prescribed standards. It is also important to note at this point that DGT can issue a letter of tax underpayment within the 5 years of incurrence of tax liability.

Tax audit in Indonesia

If DGT finds out that a company is underpaying the tax it may conduct a tax audit. Tax audit is a long process and companies should always ensure that DGT does not audit them. Apart from underpayment of taxes, there are several other reasons that can trigger the tax audit which is given below:

- A company requests a tax refund due to overpayment of tax. DGT will conduct a tax audit before making a refund.

- If a company is claiming that it has made a loss which is deemed suspicious by the DGT.

- The taxpayer has made a significant change such as a change in its year-end.

- A company fails to file the tax return and files the tax return after the issuance of a warning letter from the tax office.

- A tax return meets certain criteria which are not disclosed by the DGT.

Tax Incentives in Indonesia

One of the main priorities of the Indonesian government is to attract foreign investment. To facilitate foreign investment into Indonesia, various tax incentives are available for business activities that can facilitate industrialization, expansion of trade, adoption of new technologies.

Industries included for tax incentives

Some of those industries are given below:

- Production of components used in medical and health equipment

- Production of components used in the engines and electrical motors.

- Production of components used in motor vehicle Oil and gas refinery sector

- Production of petrochemicals from oil, gas, or coal

- Production of inorganic chemicals

- Production of organic base chemicals from agricultural and forest

- Raw materials used in the pharmaceutical

- Production of components for aircraft industry

- Production of components used in the locomotive industry

- Power plant and machine industry

- Economic infrastructure.

- Production of semiconductors and other electrical components

- Production of the components used in the smartphones industry

- Industry of upstream basic metals

- Production of components used in robots.

- Production of components used in the vessel industry

Tax allowances for companies in Indonesia

Some of the tax allowances available to companies that invest in selected business activities are as follows:

- Reduction in the taxable income of up to 30% of the investment charged over 6 years at 5% per year.

- Accelerated depreciation on tangible fixed assets and amortization on non-tangible fixed assets.

- Ability to carry forward the losses for up to 10 years.

- Withholding tax on dividends payable to shareholders abroad of 10% unless a lower tax rate is available because of double-tax treaty.

MAM Corporate Solutions can assist with corporate tax administration

Tax compliance is critical and lies at the heart of well-functioning companies. MAM Corporate Solutions has extensive experience helping clients with tax compliance in Indonesia.

Our team of tax experts are well versed with Indonesian tax laws and whether you need assistance with tax registration, payment of tax obligations on time, filing of timely tax returns, advice on the withholding taxes or correspondence with the DGT on any other tax matter, our team can assist you in all tax-related matters to ensure that not only you comply with all the tax laws but also that you are never penalized for any non-compliance.

With increasing scrutiny of individual & corporate tax administration and more frequent tax audits, it is critical to maintaining an accurate record of business transactions and taxes on monthly basis to be able to file the annual corporate tax on time. MAM Corporate Solutions offers various Monthly Accounting & Tax Compliance packages to meet the needs of its clients. You may sign up for one of our Monthly Accounting & Tax Compliance packages to ensure proper maintenance of records.

Contact MAM Corporate Solutions

If you are seeking assistance with corporate tax administration in Indonesia, you can contact our expert anytime by Clicking here or provide below as much detail about your inquiry as possible below to receive the most relevant response.

Latest insights

If you want to meet and discuss, you can easily make an appointment here.

Thanks to the efforts of the MAM Corporate Solutions team, we can now sell our products under the banner of the incorporated company. We appreciate how the MAM Corporate Solutions’ team is responsive and informative. The team’s best asset is their consistent communication.